Medicare Supplement Plan A: Navigating Your Healthcare Coverage

Navigating the complexities of healthcare coverage can be daunting, especially as we age. Medicare, a cornerstone of senior healthcare in the United States, provides crucial coverage, but it doesn't cover everything. This is where Medicare Supplement plans, often called Medigap, come into play. Among these plans, Plan A stands out as a foundational option. Let’s explore Medicare Supplement Plan A benefits and how they can contribute to your peace of mind.

Medicare Supplement Plan A provides a safety net, helping to manage the out-of-pocket costs associated with Original Medicare (Parts A and B). These costs can include copayments, coinsurance, and deductibles. By understanding what Plan A covers, you can make informed decisions about your healthcare finances and ensure you have the necessary protection when unexpected medical expenses arise.

Choosing the right Medigap policy is a personal journey, and it’s essential to understand the various options available. Plan A offers a core set of benefits, making it a popular choice for those seeking basic coverage. However, other Medigap plans offer additional benefits, and weighing these options against your individual needs and budget is a critical step in securing comprehensive healthcare coverage.

Medicare Supplement insurance policies are standardized, meaning that Plan A benefits are the same regardless of the insurance company offering the plan. This uniformity simplifies the comparison process, allowing you to focus on factors like customer service and premium costs when selecting a provider. Remember, finding the right fit involves considering both coverage and the reputation of the insurer.

Exploring the history of Medigap policies reveals a commitment to enhancing Medicare coverage and providing individuals with more financial security in the face of healthcare expenses. Plan A, as a foundational plan, has played a vital role in this evolution, offering a basic level of coverage that addresses some of the most common out-of-pocket costs associated with Original Medicare.

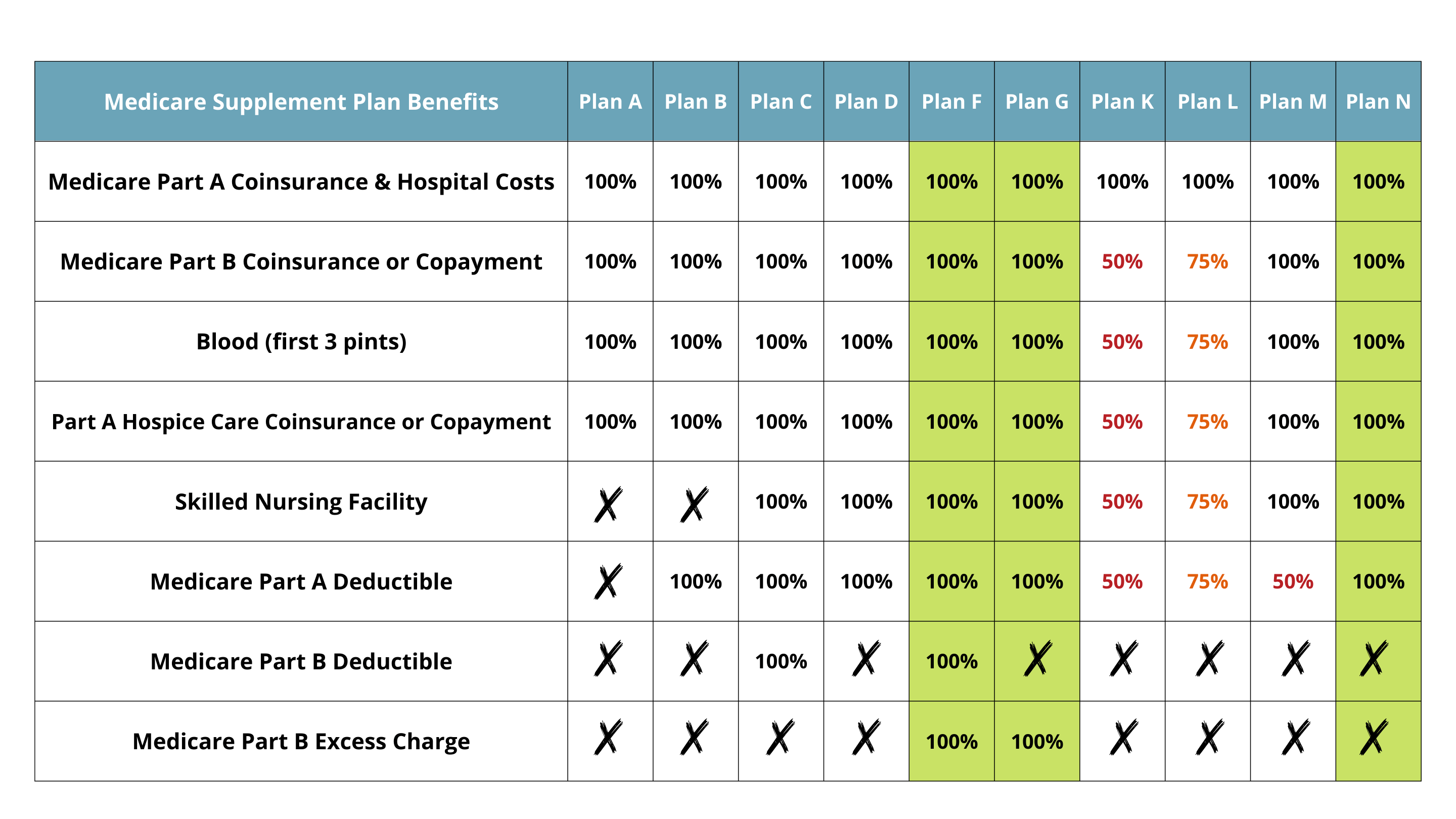

Medicare Supplement Plan A covers the following: Part A coinsurance and hospital costs (up to an additional 365 days after Medicare benefits are used up), Part B coinsurance or copayment, the first three pints of blood needed for a medical procedure, and Part A hospice care coinsurance or copayment. For example, if you're hospitalized, Plan A will cover the coinsurance costs that Original Medicare doesn't, lessening your financial burden.

One significant challenge with Plan A is that it doesn't cover Part B excess charges. This means that doctors who don’t accept Medicare’s assignment can charge up to 15% above the Medicare-approved amount, and Plan A won't cover this difference. A potential solution is to consider other Medigap plans that do offer this coverage.

Three key benefits of Plan A include predictable healthcare costs, simplified budgeting, and protection against high out-of-pocket expenses associated with hospital stays and certain medical services.

Advantages and Disadvantages of Medicare Supplement Plan A

| Advantages | Disadvantages |

|---|---|

| Covers core Medicare cost-sharing | Doesn't cover Part B excess charges |

| Predictable out-of-pocket expenses | Limited coverage compared to other Medigap plans |

Frequently Asked Questions:

1. What does Medicare Supplement Plan A cover? (Answer: Core Medicare cost-sharing such as Part A and B coinsurance, and Part A hospice care.)

2. How much does Plan A cost? (Answer: Varies by insurer and location.)

3. Who is eligible for Plan A? (Answer: Generally, individuals enrolled in Medicare Parts A and B.)

4. Can I switch Medigap plans later? (Answer: You may be able to switch plans, but it depends on various factors, including your state's regulations and the insurance company's policies.)

5. What is the difference between Medicare Supplement Plan A and other Medigap plans? (Answer: Plan A offers core benefits, while other plans provide additional coverage like Part B excess charges or foreign travel emergency care.)

6. What is the open enrollment period for Medigap? (Answer: The six-month period that starts when you’re 65 or older and enrolled in Medicare Part B.)

7. How do I choose the right Medigap plan? (Answer: Consider your healthcare needs, budget, and available plans in your area.)

8. Where can I find more information on Medicare Supplement plans? (Answer: Medicare.gov)

Tips and Tricks: Compare plan premiums from different insurers, consider your healthcare needs and budget, and review plan benefits carefully.

Understanding Medicare Supplement Plan A benefits is a critical step towards managing your healthcare finances and ensuring adequate coverage. While Plan A offers a solid foundation by covering core Medicare cost-sharing, it's important to weigh its limitations, such as the lack of coverage for Part B excess charges. Comparing Plan A with other Medigap options allows you to make an informed decision that aligns with your individual needs and financial situation. Empowering yourself with this knowledge allows you to navigate the healthcare landscape with confidence and ensure you have the protection you need to maintain your health and well-being. Taking the time to research and compare options is an investment in your future health security. Remember to consult with a licensed insurance agent or visit Medicare.gov for personalized guidance.

Conquer decimal arithmetic adding and subtracting decimals made easy

The allure of anime guys why we love ranking our favorites

Hear no evil see no evil skeletons a deeper look at the meaning history

Act NOW Dont Lose Coverage with Medicare Plan F Going Away | Innovate Stamford Now

Medicare Supplement Plan Comparison Chart 2022 | Innovate Stamford Now

Medicare Part A Deductible 2024 Benefit Period | Innovate Stamford Now

Chart Supplement User Guide | Innovate Stamford Now

Devoted Health Medicare Advantage Plans 2024 Florida | Innovate Stamford Now